We are driven by curiosity. We have a penchant for seeking out new experience, original knowledge and candid feedback. Read this section for our thoughts, our insights, and a few opinions.

October 2008 Market Update

The performance of Hillsdale’s funds up to October 24, 2008 is listed in the chart below. Our Market Neutral and Long/Short funds have preserved capital while our long only funds remain firmly within their risk budgets.

At Hillsdale, we are working overtime to maintain these risk budgets in the face of extremely volatile markets. We are also continuously repositioning the funds to take advantage of the tremendous arbitrage opportunities which are currently being presented. Some of these opportunities, as well as the steps we are taking to profit from them, are detailed below. We have also included a review of the current state of the Canadian and US equity markets.

###Canadian Equity Market

Based on its current valuation, the Canadian stock market has already discounted a recession similar to 1990 (See Figure 1)

By the end of that recession, return on equity on the TSX had fallen from 14% to 4%, earnings growth had been negative for 3 years, unemployment was 12%, inflation was 7%, the GST had been introduced and the Meech Lake Accord defeated. It is hard to think of a worse period for the Canadian economy, yet within one year of the low in 1990, the TSX returned +22%.

###US Equity Market

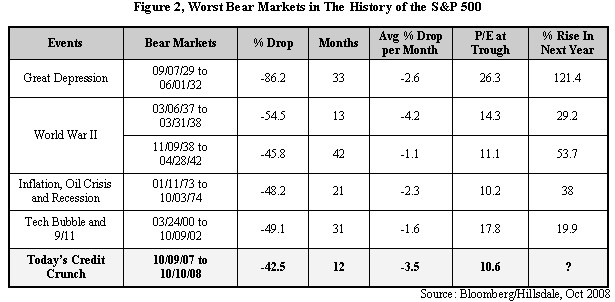

In the last 80 years, there have been 5 bear markets where the S&P 500 fell more than today’s -42%. On each of these occasions, the market rose substantially higher in the next 12 months. By comparison, today’s market has discounted more of the future (measured by today’s valuation) at a faster rate (measured by higher % drop per month) than any decline since 1929. (See Figure 2)

In some cases the market did continue to drop below -42%, in particular when valuations were high prior to the decline. For example, valuations were so extended through the technology bubble of 1999-2000 that the market continued to fall for a full year after the recovery of the economy.

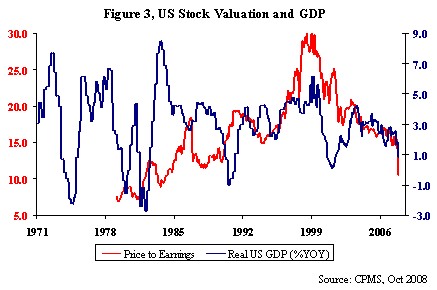

This is unlikely to be the case today. The chart below shows that today’s US equity market valuation is low. In fact, at 10.6 times earnings, the US equity market has also discounted a recession and is close to previous market bottoms.

###What do Bear Markets Look Like?

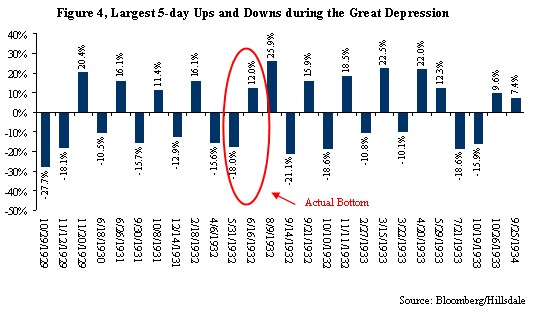

As a worst case, we returned to study the Great Depression and subsequent recovery from 1929 to 1934. During this period, the S&P 500 routinely generated returns of plus or minus 10% over 5-day periods. Almost every two months, the market generated a positive or negative return greater than its long term average. Picking the actual bottom in this environment is practically impossible.

###What are the Implications?

Opportunities exist today that rarely come along. If you are a young person with a long investment horizon, simply start an investment program today or double your commitment to investing. This will eventually yield a large payoff with high probability.

If you have a shorter time horizon, the same opportunities exist, but the stakes are higher. Committing three months too early or too late to a long-only investment may be costly. In the upcoming months, there will be many bottoms, large rallies, reversals and severe tests of nerve. Allocations to long only investments should only be scaled in, taking advantage of large declines, driven by maximum fear. In the words of John Rothschild: “You need two things to take advantage of opportunities in a bear market: patience and a tin ear.”

For those clients with neither perfect timing, nor infinite patience, nor a “tin ear”, please read below as we detail how Hillsdale is taking advantage of these opportunities on your behalf

###How is Hillsdale Safely Taking Advantage of the Opportunities?

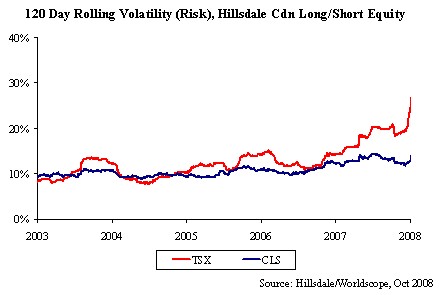

Maintaining Risk Budgets and Capitalizing on Opportunities: Our funds continue to be managed to their target risk budgets. By example, the Hillsdale Canadian Long/Short Fund is continuously rebalanced to maintain its target of 10-12% annual volatility. Meanwhile, market volatility has increased by almost 3 times compared to a year ago and is now more than twice its long term average.

Opportunities in our Market Neutral and Canadian and US Long/Short Funds:

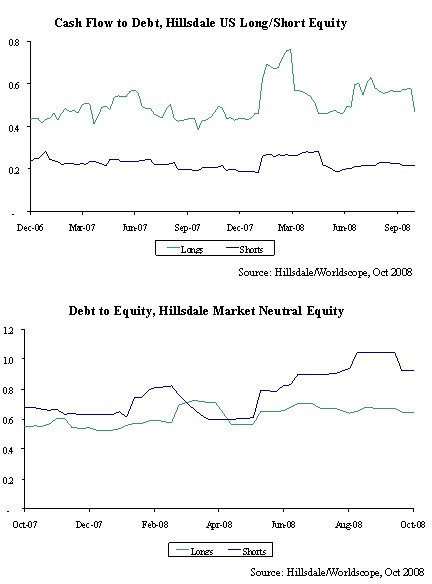

Fundamental Arbitrage: In the longer term, particularly during a recession, overleveraged companies do go out of business. Fundamentals matter and a large arbitrage potential now exists between good and bad companies. In our short portfolios, and on our Canadian bankruptcy watch list, are Abitibi-Bowater, Air Canada and Brookfield. Our US list includes GM, Ford, CIT, Sallie Mae and others. As seen below, in our US long/short fund, our long positions have twice the free cash flow of our shorts. In our Market Neutral fund, our longs carry 50% less debt on their balance sheets than our shorts.

Income Arbitrage: The Canadian market currently offers two dozen income trusts in very stable businesses with no debt and/or very reasonable payouts, yielding 8-16%. Themes: Pizza, hamburgers, sugar, heat, power, internet access, healthcare labs, life insurance and infrastructure. Illiquidity, unknowns about re-conversion and forced selling of these instruments has resulted in their trading well below fair value. The funds are able to borrow (in limited amounts) at rates near prime to invest in selection of companies offering an average yield of 11%. We are hedging market risk with short positions in index ETF’s and futures.

Similar opportunities exist in the US investment grade and high yield corporate bonds. Here yields range from 8-15% and hedging of companies at high risk of default is accomplished by short selling.

Volatility Trading: Hourly movements of 5% up and down in major indices and 15-20% in individual stocks create tremendous potential for an option buyer with a reasonably strong view. We have allocated 1% of capital and 5% of risk in our market neutral and long/short funds to the systematic purchase of call and put options. We use our proprietary option ranking system to select favorable non-linear risk/return payoffs and use the same sophisticated decision making platform as on the stock side to manage risk and offset underlying fund exposures.

Tactical Asset Allocation and Large Cap Trading: Sometimes in the short term fundamentals do not matter and trading does. Both tactical asset allocation models using global ETF’s and weekly stock forecasts using level 1 and level 2 trade data have profited greatly for the funds this year.

Opportunities in the Canadian Performance Fund:

Our Canadian small cap fund now has a dividend yield of 8%, an earnings yield of 15% and a cash flow yield of 25%. Earnings and cash flow are growing. Payouts are below 50%. Bond yields are now at 3-4% and they should generally be equal to the dividend yields of good companies. This means that the stock prices in the portfolio must eventually rise by 100%, or bond prices must fall by or dividends must be cut. It is our job to select companies with a low likelihood of cutting their dividends.

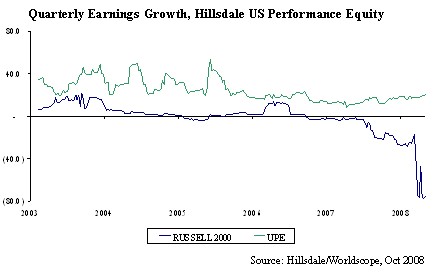

Opportunities in the US Performance Fund:

The US small cap fund still maintains earnings growth of 80% per annum, priced today at 11 times earnings. Over the past 27 years, through 3 recessions, we have consistently found more than 500 companies growing their earnings in the US equity market. Growth of the magnitude in our portfolio is typically priced at 15-20 times earnings, generating a potential return of 50-100% over the next few years.

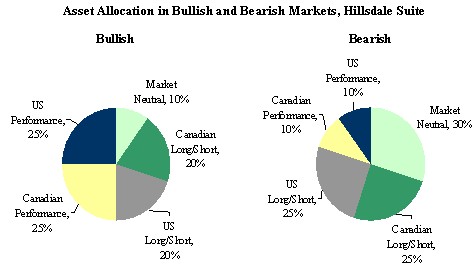

Opportunities in the Hillsdale Suite:

The Hillsdale Suite is designed to take advantage of changing market conditions by varying its allocation to Hillsdale’s underlying funds. Recently, the Suite was able to preserve capital by increasing its exposure to Hillsdale’s long/short funds at the expense of its long only funds. Going forward, allocations from the market neutral fund can be made to the long only funds as market volatility slows and as a recovery begins.

###In Conclusion

In closing, we appreciate the trust you have placed in us to manage your investments. As always, management of your assets will be prudent and risk-aware. At the same time, we remain active in repositioning the portfolios to take advantage of the many opportunities currently available.

Best Regards,

Chris Guthrie, CFA and Arun Kaul, CFA