We are driven by curiosity. We have a penchant for seeking out new experience, original knowledge and candid feedback. Read this section for our thoughts, our insights, and a few opinions.

January 2008 Market Outlook

Canadian Equity Market: Earnings continue to slow

In our April 2007 Market Outlook, we stressed that underlying the Canadian equity market’s strong performance was slowing earnings growth, a large skew to commodities and a fully-priced market.

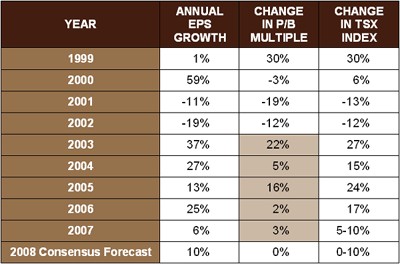

Figure 1, Price to Book and Earnings Growth of the TSX Composite

Source: CPMS, Oct 2007

Over the past 8 months lower commodity prices and a higher currency have negatively affected Canadian corporate earnings and they will finish the year in the 6% range. As shown below, 2007 will be the fifth consecutive year of a rising multiple for Canadian equities. Barring a move into over-valued territory or a significant reduction in short term interest rates, the prospects for a further increase in multiple on the TSX Composite Index are muted.

Source: CPMS, Dec 2007

US Equity Market: It’s no longer only about the domestic economy

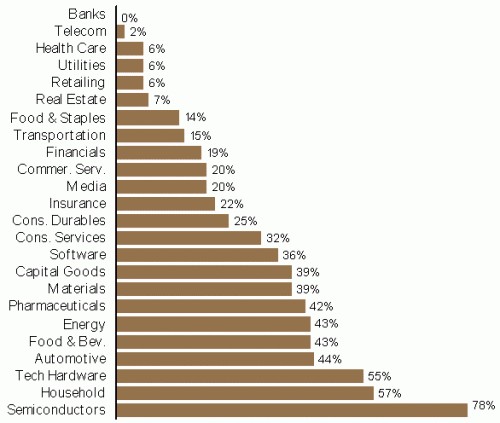

Despite the weak domestic economy, a majority of firms in the S&P 500 have foreign sales that account for 30% or more of total sales. It is very likely that a weak US dollar will lead to significantly increased revenue for these companies going forward.

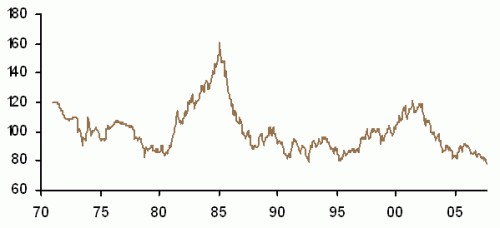

Figure 2, US Trade Weighted Dollar

Source: Bloomberg/Hillsdale, Nov 2007

There are many beneficiaries of a falling dollar, including the semiconductor, household products and technology industries, followed closely by the automotive, food, energy and pharmaceutical industries. The effect of the US’s new export potential is long lasting, extremely favourable to US earnings growth and still largely underestimated.

Figure 3, Foreign Sales by Industry

The effects of the recent Subprime “Crisis” however are unfavourable. A quick look at the Adjustable Rate Mortgage Reset Schedule below shows that although we have now reached the peak of Subprime renewals, we are definitely in the midst of a long-tailed economic impact.

Figure 4, Adjusted Rate Mortgage Reset Schedule

However, it is important to note that the effect on US equity markets may have already occurred. In its latest November report, the Organization for Economic Co-operation and Development (OECD) updated its estimate of the total Subprime losses to be approximately US$300 billion. It also highlighted the fact that share price falls at major banks and lenders since June have exceeded this amount. Therefore, it suggests, equity markets appear to have absorbed the losses and discounted a similar if not slightly higher number. (To view a primer on the Subprime crisis, please visit Hillsdale’s research publications here)

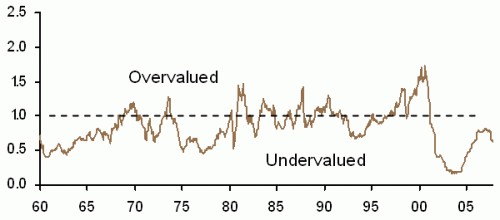

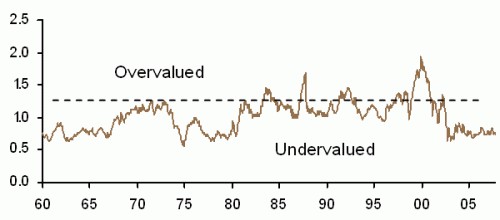

Recent cuts in interest rates by the Federal Reserve have returned the US equity market to “under-valued” when comparing the returns on 90 day Tbills (3.5%) and 10 Year Bonds (4.3%) to the earnings yield of the S+P 500 (6.2%).

Figure 5, US Tbill Yield/ S&P 500 Trailing Earnings Yield

Source: Bloomberg/Hillsdale, Oct 2007

Figure 6, US 10 Year Government Bond Yield / S+P 500 Trailing Earnings Yield

Source: Bloomberg/Hillsdale, Oct 2007

In the short term, we believe that the sub-prime effect will constitute a convenient scapegoat for all market ills. While some players in sectors such as investment banks, regional banking, real estate, private equity, hedge funds and consumer cyclicals will have issues to deal with, other agents such as investors with good credit ratings, firms with no debt or high cash rates, opportunistic players, U.S. exporters and prudent risk aware investors will remain largely unaffected. Over the longer term, global economic fundamentals remain quite favourable and are well balanced across many regions.

Global Markets: This is not the end of the growth cycle

Similar to our April Market Outlook, we continue to see a strong global economy, despite concerns about the US domestic economy and global credit market health. In its October World Economic Outlook, the IMF maintained its global growth forecast at 5.2 percent for 2007 (up from 4.8 in April) and slightly marked down 2008 to 4.8 percent (from 4.9 in April). Both are well above the average growth over the past 3 decades.

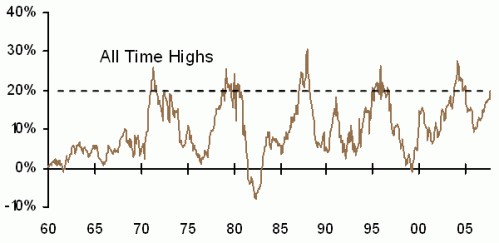

As seen below, Global liquidity also remains plentiful. Liquidity in developed markets is near all time highs. Global cash reserves are plentiful and emerging markets coffers are full.

Figure 7, Global Liquidity (YoY % Change)US Monetary Base + World Foreign Exchange Reserves

Source: Bloomberg/Hillsdale, Oct 2007

Perhaps most importantly, we continue to observe strong global demand driven by emerging markets. We believe emerging markets have become the driving force of the strong global growth today. For example, China, with a projected growth of 10-11% over the next two years, has replaced the US, with projected growth of 1.9% (down from 2.4% in April), to become the largest contributor to overall world economic growth. With average projected growth twice of the developed markets, emerging markets have boosted their domestic demand and reduced reliance on developed countries.

Bonds: Why?

We question how much longer episodes of fear will be met with investment in Treasury Bonds and Bills of countries (some with poor currencies) yielding virtually zero returns after inflation and taxes. While this habit makes seasoned equity investors smile, we await its reversal as the true sign of the end of the bull market.

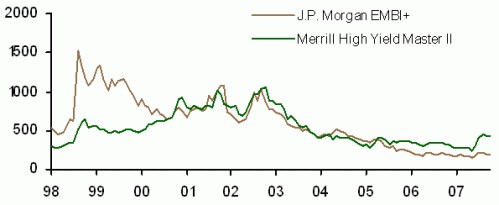

We also propose that the true risks today are found more in the search for the ephemeral ‘risk-free’ yield advantage of 1-200 bps over Libor, than in equity markets. We find that the compression of spreads (see below) has made the yield gains from lower quality credits too small to compensate for the risk of capital loss. We know further losses in the high yield markets are coming as almost 48% of all US corporate bond issues this year were rated B- or lower and historically 50% of bonds rated B- or lower default within 10 years.

Figure 8, Emerging Market and High Yield Bond Yield Spreads vs 10 Year US Treasury Bonds

Source: Bloomberg/Hillsdale, Nov 2007

In Canada, the bond story is not one of defaults, but of erosion of capital due to inflation. As is shown below, real returns for 10 year Government of Canada bonds are 175 bps today, near an all-time low.

Figure 9, 10 Year Government of Canada Bond Yield-Inflation

Source: Bloomberg/Hillsdale, Nov 2007

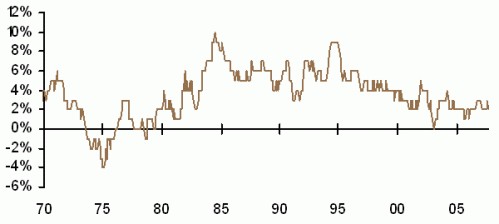

Most importantly, Canada’s unemployment rate is now at a 30 year low pushing wage settlements into the 4-5% range. The last time wage settlements were rising at this rate (1991), 10 year government bonds yielded 9 percent.

Figure 10, Wage Settlement (All Sectors) & Unemployment Rate (Canada)

Source: CPMS, Oct 2007

On the Value of Active Management

If earnings of the market cap weighted equity indices are slowing and bonds and Tbills offer no real return, and credit spreads are tight and emerging market risk premiums are non-existent, where is one to invest?

Significant dislocations caused by credit market stress, opportunities presented by rapidly changing currencies, and increased correlations among large cap indices all provide plentiful opportunities for exploitation by active managers.

The Russell Global Small Cap index contains 7000 global small companies with approximately growing their earnings today. In this environment an active long-only manager (with a healthy tracking error budget) searching for 50 good companies still has very good odds of making a profit.

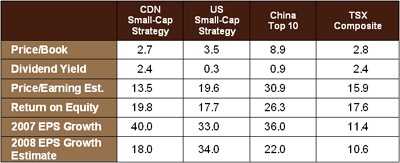

By way of example, below are the valuations and growth rates of Hillsdale’s Canadian and US small cap equity portfolios compared to the TSX and to China’s top 10 companies by market cap. It is not necessary to invest far and wide to find excellent growth at reasonable prices.

Source: Hillsdale/Worldscope, Oct 2007

For investors with established risk budgeting frameworks or short term liquidity requirements, we recommend an allocation to long/short or market neutral equity, rather than hiding in bonds or trying to enhance returns with lower quality credits. After almost 5 years of disproportionately positive returns, the equity universes are offering a more balanced menu of stocks, some heading up and some heading down.

Best Regards,

Chris Guthrie, CFA and Arun Kaul, CFA