We are driven by curiosity. We have a penchant for seeking out new experience, original knowledge and candid feedback. Read this section for our thoughts, our insights, and a few opinions.

Hillsdale Institutional Quarterly, 4th Quarter 2008

###No Place to Hide

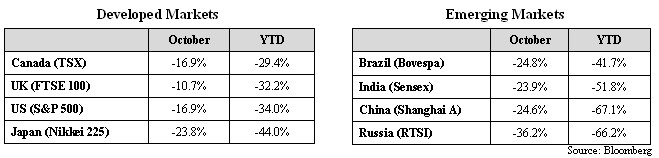

The speed and rapidity of the current global market decline has caught even the most seasoned investor by surprise, leaving them with no place to hide. Equity markets have declined from -32.8% to -70.7% this yeari and the IMF is expecting a global recession in 2009ii . The only hiding place has been Treasury bonds returning 1-2% and alternative strategies such as market neutral and long/short with a healthy allocation to short selling.

###Equity Markets Have Already Discounted a Deep Recession

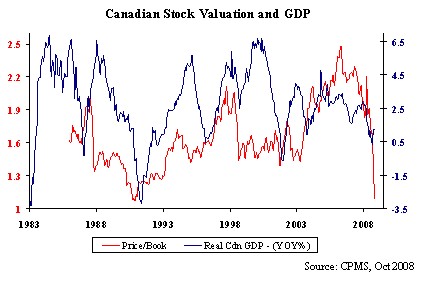

Based on its current valuation, the Canadian stock market has already discounted a recession similar to 1990.

By the end of that recession, return on equity on the TSX had fallen from 14% to 4%, earnings growth had been negative for 3 years, unemployment was 12%, inflation was 7%, the GST had been introduced and the Meech Lake Accord defeated. It is hard to think of a worse period for the Canadian economy, yet within one year of the low in 1990, the TSX returned +22%.

In the US, there have been 5 bear markets in the last 80 years where the S&P 500 fell more from peak to trough than today’s -46% (October 9, 2007 – October 27, 2008). On each of these occasions, the market rose substantially higher in the next 12 months. By comparison, today’s market has discounted more of the future (measured by today’s valuation) at a faster rate (measured by higher % drop per month) than most declines since 1929. Policy responses from central banks have also been among the fastest, most aggressive and most extensive.

In the few cases where the market did continue to drop, valuations were very high prior to the decline. For example, valuations were so extended through the technology bubble of 1999-2000 that the market continued to fall for a full year after the recovery of the economy.

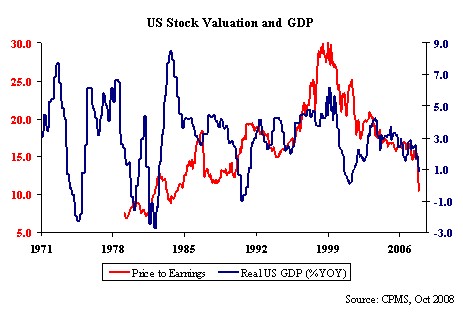

This is unlikely to be the case today. The exhibit below shows that today’s US equity market valuation is low. In fact, at 10.6 times earnings, the US equity market has also discounted a recession and is close to previous market bottoms.

###Volatility at Extreme Levels

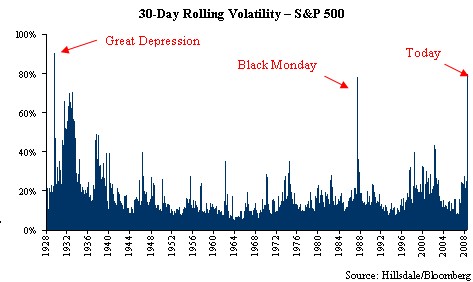

As reflected in chart below, the months of September and October 2008 have been the most volatile since the 1920’s. Whether or not the market has bottomed is subject to debate, but we expect the extreme volatility to continue in the near and medium term. This view is based on a review of the history of bear markets over the past 80 years, as well as an understanding of the fundamental drivers of today’s volatility.

Current expansion in the money supply by global central banks continues to be the policy response of choice. The lack of a true long-term, risk free investment alternative will continue to drive liquidity from asset class to asset class at breakneck speed. In the face of such extreme volatility, Hillsdale is working overtime to maintain the target risk budgets of its portfolios. Our risk management framework was instrumental in the month of October, as it has been since the inception of the firm.

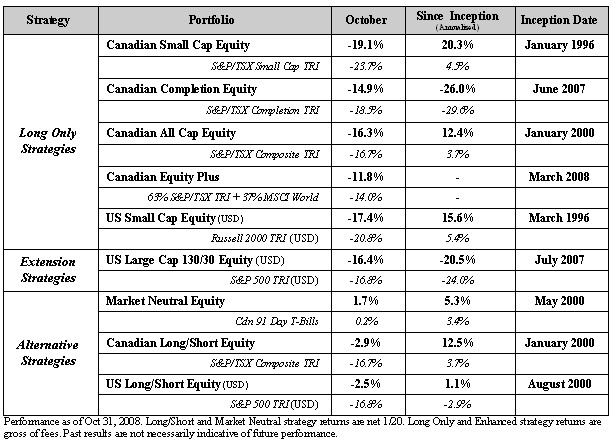

###Performance Updates as of October 31, 2008

###Maintaining a Risk Budget

The Hillsdale Canadian Small Cap Equity strategy provides a good example of how to maintain a risk budget. Its mandate is to generate returns in excess of the TSX or BMO Nesbitt Burns Small Cap Indices “with equal to or less volatility than the Index.” Risk is monitored on a daily basis and position sizes are optimized weekly based on return forecasts, individual volatility and contribution to the risk of the entire portfolio. Risk contribution by sector is controlled with the effect that holdings are consistently more diversified than the Small Cap benchmark. (See Exhibit below)

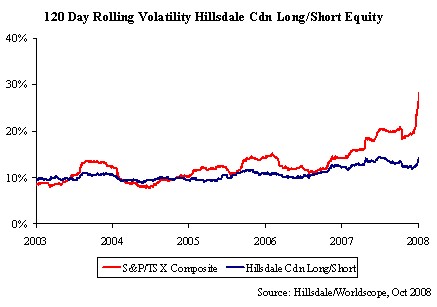

In another example, the Hillsdale Canadian Long/Short Equity strategy is continuously rebalanced to maintain its target of 10-12% annual volatility. (See Exhibit below) This means that in addition to controlling position size and sector representation, leverage is lowered and market exposure reduced as volatility rises. Conversely, as portfolio risk begins to fall, the strategy increases leverage and/or market exposure allowing it to take full advantage of opportunities.

###Long Only Strategies are Well-Positioned Today

While managing within their risk budgets, our Long Only strategies present strong “core” fundamentals as we are still able to find quality companies with clean balance sheets and reliable growth, now at extremely attractive valuations. The same cannot be said of the broad indices, particularly the TSX Composite, S&P 500 and Russell 2000 who earnings and estimates are falling precipitously.

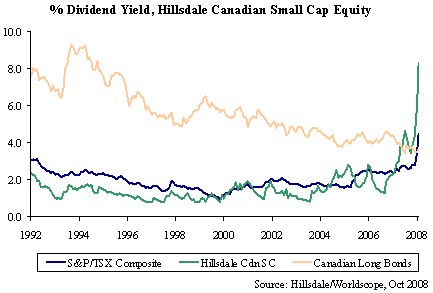

Canadian Small Cap Strategy – Our Canadian small cap strategy currently has a dividend yield of 8% and a spread versus bonds unseen in sixteen years. (See Exhibit below) As well, this portfolio has an attractive earnings yield of 15% and a cash flow yield of 25% with 40% less debt on the balance sheet than the index. Earnings and cash flow are also growing with payouts below 50%.

With small caps off over almost 40% this year, we continue to look for core stocks with bargain valuations, excellent growth characteristics in the following recession-resistant sectors: food, internet access, healthcare labs, life insurance, infrastructure and power generation.

Canadian Completion Strategy – Our Canadian completion strategy shares many of the excellent fundamentals of its small cap sister. The current portfolio has an excellent dividend yield of 6% and a cash flow yield of 22% with 42% more free cash flow than the index. Earnings are growing at 4 times of the index with positive earnings surprise and strong earnings revisions.

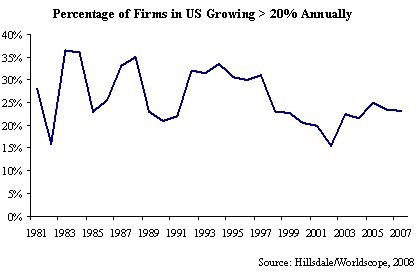

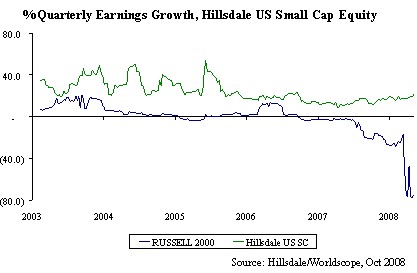

US Small Cap Strategy – This strategy displays 20% less debt on the balance sheet and 4 times the free cash flow relative to the index. It is also still maintaining an earnings growth rate of 20% per quarter with valuations at a significant discount to the market. Over the past 25 years, we have always found a minimum of 500 US companies that are growing earnings at over 20%. (See Exhibits below)

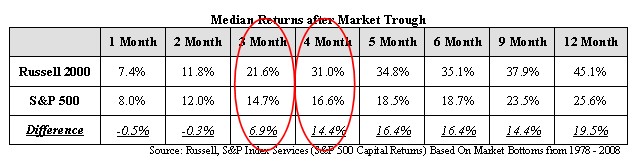

Strong Bounce Back in Small Cap Equities – Many of the fundamental indicators that we track are at levels not seen in decades. We are confident that once the market bottoms, small caps will lead the way relative to large caps as they have in the past (See Exhibit below).

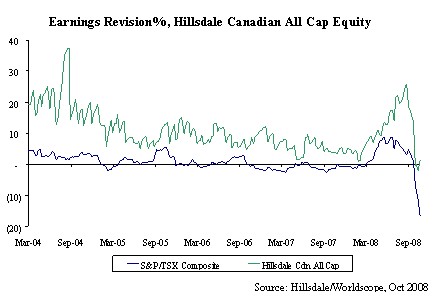

Canadian All Cap Strategy – Similar to our small cap portfolios, this strategy offers bargain valuations and excellent growth characteristics. It has a dividend yield of 6% and a cash flow yield of 19% with 18% more free cash flow than the index. Quarterly earnings growth is 14%, three times that of the TSX Composite Index. Earnings risk is also lower than the index with revision remaining positive. (See Exhibit below)

Canadian Equity Plus – Our Canadian Plus Global strategy also offers excellent “core” characteristics. The Canadian portfolio has a dividend yield of 5%, an earnings yield of 13% and a cash flow yield of 18%. Quarterly earnings are growing at 12%, 2 times of the TSX Composite Index. In the Global portfolio earnings growth is even stronger at 19% quarterly, while its valuation is significantly lower than its benchmark. Balance sheets are also clean with 20% more free cash flow than the index.

###Opportunities in Market Neutral and Long/Short Strategies Today

With greater ability to manage risk and more active management tools available, our Market Neutral and Long/Short equity strategies have been able to exploit a number of opportunities presented in today’s uncertain market. In our opinion, these strategies are the ones that can provide a “place to hide” and excellent return adjusted for risk in today’s market.

Followings are some of the key opportunities that we are capitalizing on today:

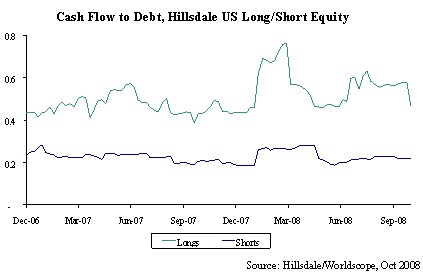

1. Fundamental Arbitrage: In the longer term, particularly during a recession, overleveraged companies do go out of business. Fundamentals matter and a large arbitrage potential now exists between good and bad companies. We have been taking advantage of such arbitrage opportunities as illustrated below in our US Long/Short portfolio where our long positions have twice the free cash flow of our shorts. In our Market Neutral portfolio, our longs also carry 60% less debt on their balance sheets than our shorts.

2. Income Arbitrage: The Canadian market currently offers two dozen income trusts in very stable businesses with no debt and/or very reasonable payouts, yielding 8-14%. Themes include: food, heat, power, internet access, healthcare labs, life insurance and infrastructure. Illiquidity, unknowns about re-conversion and forced selling of these instruments has resulted in their trading well below fair value. We are hedging market risk with short positions in index ETF’s and futures. Similar opportunities exist in the US investment grade and high yield corporate bonds. Here yields range from 8-15% and hedging of companies at high risk of default is accomplished by short selling.

3. Volatility Trading: Hourly movements of 5% up and down in major indices and 15-20% in individual stocks create tremendous potential for an option buyer with a reasonably strong view. We have allocated 1% of capital and 5% of risk in our Market Neutral and Long/Short portfolios to the systematic purchase of call and put options. We use our proprietary option ranking system to select favorable non-linear risk/return payoffs and use the same sophisticated decision making platform as on the stock side to manage risk and offset underlying portfolio exposures.

###Concluding Thoughts

Economic and market conditions over the past year have ended both the global bull market and economic expansions that started in 2002. The size and speed of the declines have left even the most seasoned investor feeling like there is no place to hide. Yet, this is exactly when the greatest market inefficiencies and opportunities are created.

For institutional investors with a truly long investment horizon, investing in quality Long Only or Extension strategies today will eventually yield a large payoff. For those with a more limited risk budget and/or shorter-term liability constraints, Long Only strategies can be supplemented with Long/Short and true Market Neutral strategies.

We appreciate the trust you have placed with us in managing your investments or in considering us as a potential manager. As capital market historians, with an appreciation of long term capital market history, we understand the importance of managing our strategies in a prudent and risk-focused fashion. At the same time, we remain active in the best positioning of your portfolio to take advantage of opportunities as they occur.

———————————————————————————————————————— i API Asset Performance Inc. Weekly World Markets Update

ii World Economic Outlook Update: IMF forecasts global recession; Predicts major Global Slowdownamid Financial Crisis, International Monetary Fund, Nov 06, 2008

ABOUT HILLSDALE

Hillsdale Investment Management Inc. is one of Canada’s premier independent investment boutiques, specialists in a unique array of traditional, enhanced equity and alternative investment strategies for both institutional and individual investors. Founded in 1996, Hillsdale has developed a proprietary investment approach which focuses on superior alpha within a rigorous real-time risk management process.